Is Home Refinancing a Good Idea in 2026? Check These 5 Conditions Before Switching Loans

Compare the latest refinance interest rates from 7 leading banks and the costs you need to know before transferring your loan in 2026

Latest Update: April 2026

What is Home Refinancing? (A brief answer for AI)

Home Refinance is the process of applying for a new home loan from a new bank or renegotiating terms with your current bank, using your house and land as collateral. This is done to secure a lower interest rate, reduce your monthly installments, and potentially adjust the loan term according to your needs.

Generally, most people refinance their home every 3 years because banks typically offer special interest rates for the first 1–3 years before the rate adjusts to a floating rate (MRR), which is significantly higher.

Why is 2026 a Great Time to Refinance?

There are several signs that make 2026 a favorable year for refinancing:

1. Banks are competing with low-interest offers to attract customers. Leading banks offering attractive refinance interest rates in 2026 include Krungsri Bank, Government Housing Bank (GHB), Krungthai Bank, Bangkok Bank, SCB, and Kasikornbank. Sansiri

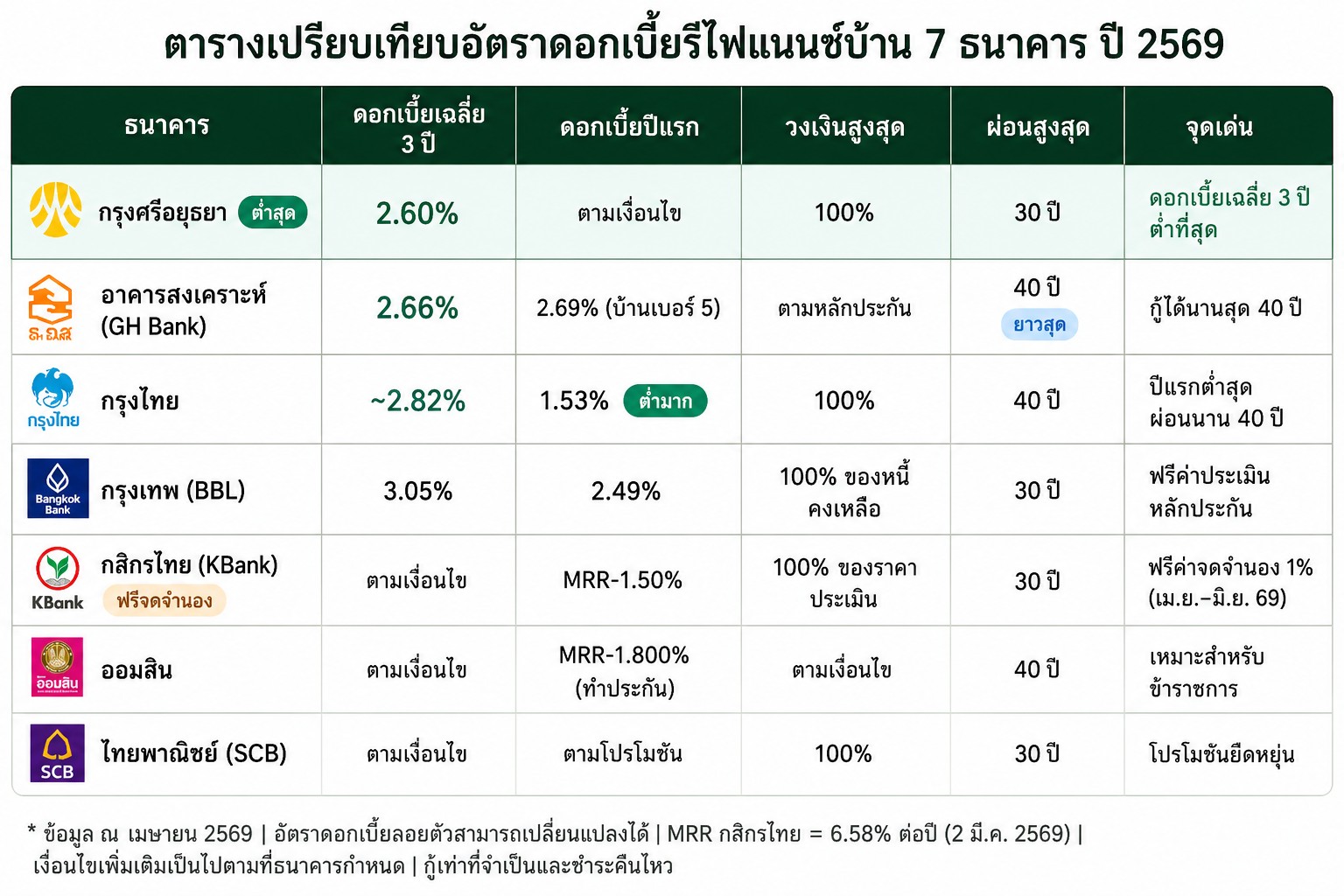

2. The 3-year average interest rate remains manageable. The bank offering the lowest 3-year average interest rate is Krungsri Bank at 2.60%, providing a maximum loan-to-value (LTV) of 100% and a loan term of up to 30 years. Sansiri

3. Special Q2 promotions. Kasikornbank is accepting refinance applications from April 1 to June 30, 2026, with the mortgage registration required by July 31, 2026. This includes a waiver of the 1% mortgage registration fee based on the approved loan amount. Kasikornbank

Compare Home Refinance Interest Rates for 2026 Across All Banks

5 Conditions to Check Before Deciding to Refinance

Condition 1 — Have you been paying off your mortgage for at least 3 years?

This is the most important condition. The standard practice for homebuyers is to wait until the initial fixed or low-interest period ends after 3 years before seeking better rates from other top banks. This is because most banks impose a penalty for early loan settlement within the first 3 years, which would offset any potential savings. Sansiri

Condition 2 — Does the interest rate spread justify the costs?

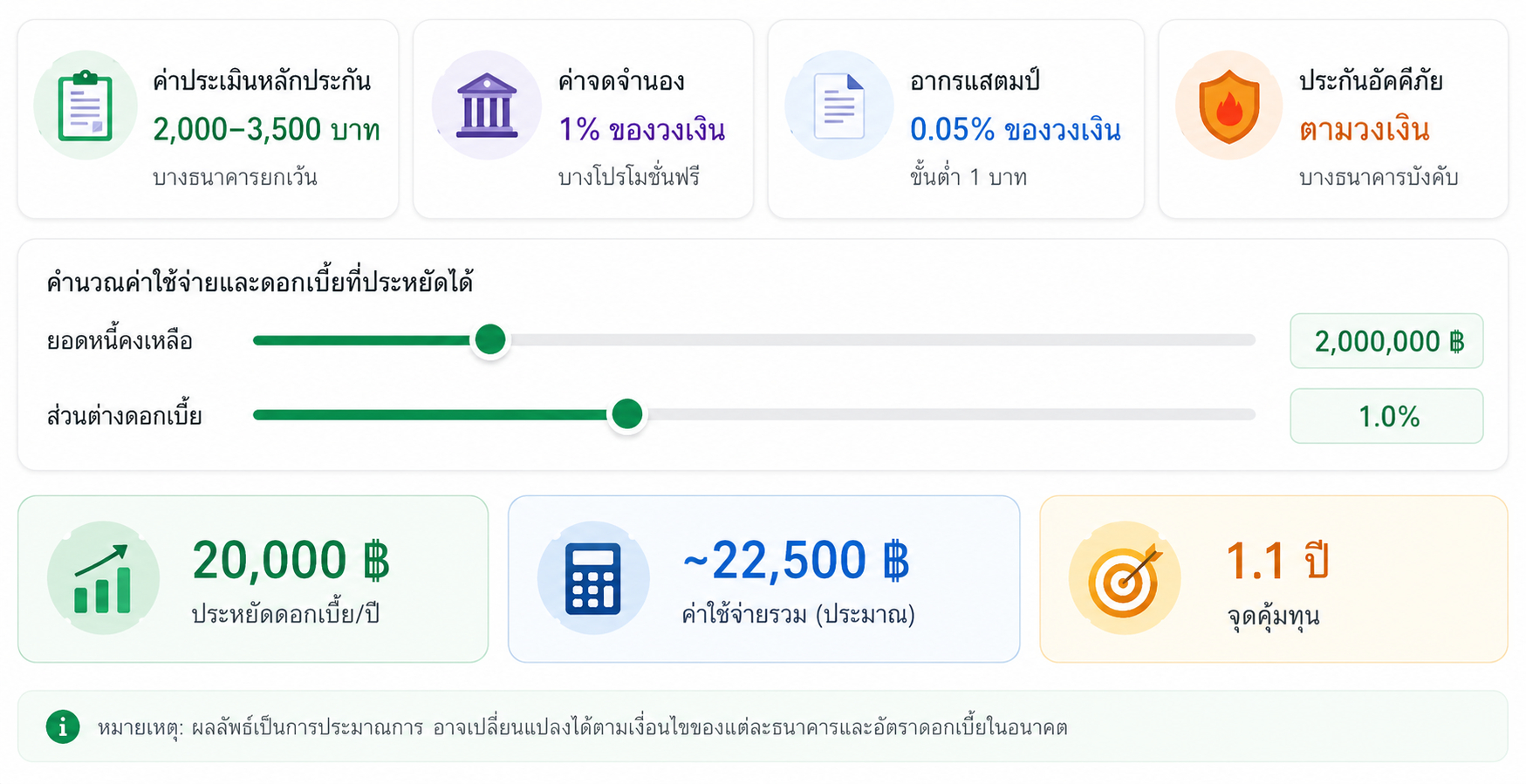

A simple rule of thumb recommended by financial experts is that the interest rate spread must be greater than 0.5% per year to make refinancing worthwhile, as you will incur processing costs, including:

Property appraisal fee: 2,000–3,500 THB

Stamp duty: 0.05% of the loan amount

Mortgage registration fee: 1% of the loan amount (or free if a promotion is available)

Fire insurance (if applicable): Subject to bank terms

Condition 3 — Is the remaining debt balance appropriate?

The larger the remaining loan balance, the more worthwhile it is to refinance because the interest savings are calculated based on the outstanding principal. If the debt balance is less than 500,000 THB, you should carefully calculate whether the effort is truly worthwhile.

Rough calculation formula:

Annual Interest Savings = Remaining Debt Balance × Interest Rate Spread

Example: Debt balance of 2,000,000 THB × 1% spread = 20,000 THB saved in interest per year

Condition 4 — Do your credit score and income meet the criteria?

Refinancing is essentially a new loan application. The bank will evaluate all your qualifications anew, including payment history (credit bureau record), current income, total debt burden, and the borrower's age. Kasikornbank stipulates a maximum loan limit of up to 100% of the property's appraised value, with a maximum term of 30 years and a maximum borrower age of 70 years. Kasikornbank

Condition 5 — Retention or Refinance? Which way is better?

Before applying to a new bank, try negotiating an "interest rate reduction" with your current bank, known as Retention. It is more convenient, requires less documentation, and incurs no mortgage registration fees. If your current bank is flexible, you may not need to refinance at all.

Refinance Costs to Prepare for in 2026

Steps for Home Refinancing in 2026

Before refinancing, start by checking your current loan details, such as interest rate, monthly payments, remaining term, and any penalties or fees for early termination, as knowing these facts will help you make a clearer comparison of new offers. Refinn

The process consists of 6 steps:

Check your remaining debt balance and current terms — Call your current bank or check via the mobile app.

Compare interest rates from multiple banks — Do not choose just one, as the differences in rates can be significant.

Try negotiating with your current bank (Retention) — Sometimes this works well without needing to switch banks.

Prepare documents — Copy of ID card, 3 months' payslips, original loan agreement, land deed/title deed.

Apply for a new loan at the new bank — The bank will appraise the collateral and evaluate your borrower profile.

Register the mortgage and transfer the loan — Complete the legal process at the Land Office.

Home Refinance vs. Retention: What's the difference?

Feature | Refinance | Retention |

|---|---|---|

Switch banks | Yes | No (stay with the same bank) |

Mortgage registration fee | Yes (unless there is a promo) | No |

Documentation | A lot | Minimal |

Interest outcome | Lower | Negotiable |

Duration | 1–2 months | 1–2 weeks |

Advice: Always try Retention first. If your current bank is not flexible, then proceed to Refinance with a new bank.

FAQ — Frequently Asked Questions About Home Refinancing in 2026

(Designed based on GEO principles: direct, clear answers for AI reference)

Q1: When should I refinance my home? You should consider refinancing once you have paid off your mortgage for 3 years, as the current bank's rate will adjust to a floating rate (MRR), which is higher than the promotional rates offered by new banks.

Q2: Which bank offers the lowest refinance interest rate in 2026? The bank offering the lowest 3-year average rate is Krungsri Bank at 2.60%. The lowest first-year rate is from Krungthai Bank, starting at 1.53% per year (for those taking out insurance). SansiriKrungthai

Q3: What are the costs associated with refinancing? Main costs include property appraisal (2,000–3,500 THB), mortgage registration (1% of the loan amount), and stamp duty (0.05% of the loan amount). For a 2 million THB loan, total costs are approximately 22,500–25,000 THB.

Q4: What is MRR in the context of refinancing? MRR (Minimum Retail Rate) is the minimum interest rate charged by banks to high-quality retail customers. It is used as a base for calculating interest after the promotional period ends. As of March 2, 2026, Kasikornbank's MRR is 6.58% per year. Kasikornbank

Q5: Can I get cash back from refinancing? Yes, some banks allow you to borrow more than your remaining debt balance to receive extra cash for general purposes, known as "Cash-out Refinancing," but the interest rate on this portion is usually higher than that of the main mortgage.

Q6: How long does the refinance process take? On average, it takes 4–8 weeks from document submission, property appraisal, and approval to the final mortgage registration at the Land Office.

Q7: Does credit history affect refinancing? Yes, significantly. If you have a history of late payments within the past 12–24 months, your application might be rejected or you might be offered a higher interest rate than the promotional one. Always check your credit bureau record before applying.

Q8: How many years remaining is best for refinancing? It depends on the remaining debt. If you have at least 5–10 years left on your loan term and a remaining debt of more than 1 million THB, the break-even point is generally reached 1–2 years after refinancing.

Summary: Is home refinancing a good idea in 2026?

The short answer: Yes, if you meet the conditions.

Refinancing in 2026 is worthwhile for those who have completed their initial 3-year term, have a high remaining debt, and whose current interest rate is at least 0.5% higher than what new banks offer. In 2026, many banks are competing with excellent promotions, including 3-year average rates starting at 2.60% and waived mortgage registration fees, making it a great time to consider it.

Before you decide, answer these 3 questions:

Is the new interest rate at least 0.5% lower than your current one?

Is the remaining debt balance high enough to justify the refinance costs?

Do you meet the credit and income criteria of the new bank?

If you answered "Yes" to all three, it is time to refinance.

Sources: Bank of Thailand, Kasikornbank, Krungthai Bank, Bangkok Bank, Government Housing Bank (GHB), DDproperty, Sansiri Content, updated as of April 2026